How would you react to the presentation of a method for measuring project performance, forecasting costs and deadlines, identifying problems and making the right decisions? The response would undoubtedly be excellent and would consign many of your current practices to oblivion!

Born at the end of the 60s in the U.S. Department of Defence, EVM (Earned Value Management) has been delivering on these promises for several decades now, but its use remains discreet in France.

How can we put this method into practice? What pitfalls should we be wary of? How can we avoid them? And what are the benefits?

All these questions deserve answers. We invite you to study the subject, using as examples first a nuclear power plant construction project, then a portfolio of industrial projects. We hope that a summary of the lessons learned will enable you to move from theory to practice!

Survival Glossary (*)

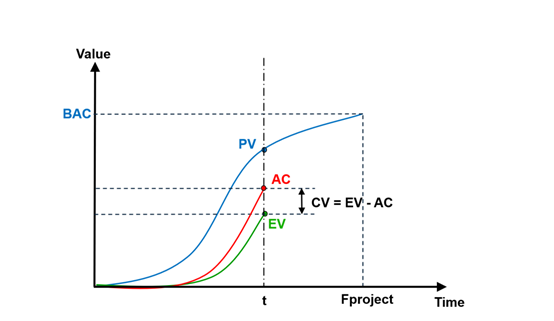

- AC = Actual Costs

- BAC = Budget at Completion

- CV = Cost Variance: CV = EV – AC

- EAC = Estimate at Completion

- EV = Earned Value: EV = ∑ (Task Budget x Task Progress)

- PMR = Project Management Reserves

- PV = Planned Value

- SV = Schedule Variance: SV = EV – PV

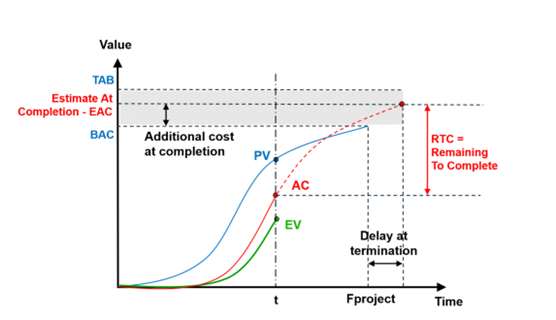

- TAB = Total Allocated Budget: TAB = BAC + PMR

(*) For a more detailed description of the method, please refer to the end of this article.

EXAMPLE: EVM ON A NUCLEAR POWER PLANT CONSTRUCTION PROJECT

PROJECT CHARACTERISTICS

The case studied is that of a project to produce execution studies (plans and models), for the construction of a nuclear power plant, by a group of companies.

The buildings to be constructed are made up of storeys, and the work sequences are well established. The project is therefore repetitive and industrial. This organization is reflected in the specifications. The budget for each task (BAC task) is known from the outset. This organization is also reflected in the project structures, with coherent WBS (Work Breakdown Structure) and CBS (Cost Breakdown Structure).

The contract requires the implementation of a process for managing developments from start of the project. It also stipulates that the financial management of changes must comply with the budgetary rules in force on the project. These provisions facilitate PV (Planned Value) maintenance.

EVM SYSTEM

The project team established common rules for measuring physical progress right from the start of the project. Particular care was taken to ensure that these rules were deployed and applied uniformly and continuously by all those involved throughout the life of the project.

From a planning point of view, the following data has been maintained in Primavera:

- Baseline schedule (initial schedule + changes)

- Project schedule up to date

Costs were re-injected into Excel, enabling the following data to be maintained:

- Budget baseline (PV) re-evaluated each month to take account of changes

- Costs incurred (AC) and estimated costs to completion (EAC).

This information was concatenated monthly in Excel to establish the EVM indicators. These indicators were injected into Power BI for better visualization.

PITFALLS AND SOLUTIONS

- As the EVM method manipulates cost data, it was approached by some project managers as a purely financial tool. The method manager for the project had to acculturate the teams to the fact that EVM is first and foremost a steering and communication tool. Even more than with other approaches, Earned Value Management requires an appropriate amount of explanation time to be devoted to the teams in charge of implementing it.

- Another stumbling block for the project was the time it took to contract out the changes. Several months passed between the validation of a change and its contractualization in the form of an order. During this time, an evolution that had been validated but not yet ordered was considered in the project status to date (EV), but not in the project baseline (PV), which only considers ordered evolutions. The SV deviation, calculated from elements that did not share the same contractual reference, therefore misrepresented the actual project situation. The solution was to set up an adjusted Baseline (PV’) incorporating, in advance, evolutions for which the contract had been acquired or almost acquired. In other words, SV’ = EV – PV’ replaced SV = EV – PV. By cancelling out the effects of contract deadlines, the use of this adjusted Baseline has made it possible to restore meaning and usefulness to project performance gap measures.

- The customer imposed an EVM on all project activities, including cross-functional activities (training, management, software licenses, etc.), which have particularities in terms of planning (e.g.: management lasts as long as the project) or acquired value measurement (what is the acquired value of management?). Specific rules therefore had to be defined to make management relevant: – Budget distribution according to the number of training sessions, or proportion to study production tasks. – Progress according to the number of sessions completed, time spent, or proportion to study production tasks.

BENEFITS

Thanks to a rigorous EVM approach, the project team and the customer had a shared view of progress throughout the life of the project. The precision of the indicators positioned discussions on the real situation of the project, its successes and risks, and made it easier to take steering actions, at the right moment, for maximum efficiency. The ability to zoom in on progress at project level or activity level enabled us to fine-tune diagnoses and action plans. Ultimately, schedule (SV’) and cost (CV) variances remained under control.

EVM FOR A PORTFOLIO OF INDUSTRIAL PROJECTS

PROJECT DESCRIPTION

The case studied is that of a portfolio of engineering projects in the industrial sector, containing several hundred projects.

EVM SYSTEM

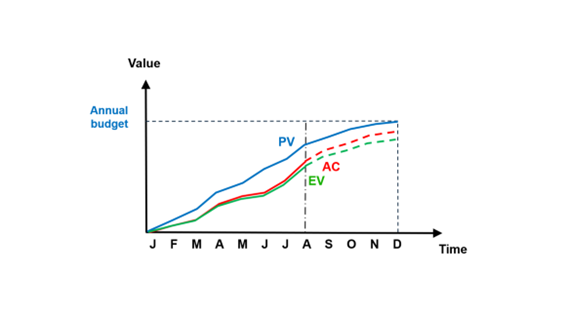

- The monitoring method used measures the project performance in relation to the annual budget. It thus differs from conventional earned value management, which refers to the budget at completion. We could therefore call this method an annualized EVM.

- This first simplification is accompanied by a second: physical progress is achieved via representative milestones sharing, in principle, the same financial weight. In this system, a project with an annual budget of €2 million, for example, will typically be represented by twenty or so milestones, each weighing €100K. The wise project manager will define his milestones in such a way that they correctly represent the budget and expenditure profile associated with the project tasks (i.e. the more a task costs, the more milestones it has).

- Modification of the project’s annual Baseline and associated PV is only authorized in the event of contractual changes involving a change in scope independent of project performance. In the absence of contractual changes, the schedule delay and/or additional costs result from lower-than-expected project performance, and Baseline modification is not authorized, thus maintaining a measurable variance thanks to EVM indicators.

- Portfolio projects are planned in a PPM (Project Portfolio Management) tool, incorporating modules specifically parameterized for annualized EVM. The tool assists: – Project managers in calculating variances (SV, CV), performance indicators (SPI, CPI) and projections of earned value (EV) and expenditure (AC) at year-end, by extending the trends observed to date. – The portfolio manager in providing visibility on the current and future performance of the project portfolio, in analysing this performance at different levels of aggregation, and in detecting under-performing projects.

PITFALLS AND SOLUTIONS

The main pitfall of this method stems directly from its founding principle, i.e. to implement an annualized EVM focused on the current year’s performance and not on the project’s terminal performance. It is thus possible for a project initially planned for five years to start its seventh year of existence with the new (and seventh!) annual PV as its performance measurement point. It’s as if at the start of each new year, the project’s performance measurement can be restarted from scratch. This mode of operation, based on a succession of annual performances, distances teams from the notion of overall project performance. While there are safeguards in the form of annual drift ceilings for the SPI and CPI indicators, what about the project that manages to stay just below the authorized threshold year after year? It’s doubtful that its overall performance will be there.

BENEFITS

The first benefit of annualized EVM is that it provides project managers with a simple, turnkey method of measuring project progress, and objectifying this measurement in relation to expenditure.

A second benefit is the reliability of budget forecasting for the portfolio’s financiers, despite the very large number of projects. The availability of monthly performance reports not only ensures accurate budget marking, but also enables a pooled support team to be activated to help the most at-risk projects implement appropriate security plans.

We might add that an annualized EVM is less demanding in terms of planning than a classic EVM. This may be worth considering if the project portfolio is regularly confronted with a lack of planning maturity, whatever the cause: complex or innovative nature of the projects, planning skills of the teams, etc.

IN CONCLUSION

What can we learn from this long presentation?

- Firstly, that it is possible (and very useful!) to deploy Earned Value Management, or a relevant adaptation of its concepts, on real projects, either large size or in large numbers.

- Secondly, that given the accumulation of constraints (method requirements, size or number of projects, etc.), it is useful to simplify the problem. This is what has been achieved in the examples presented. The nuclear power plant construction project is based on the recurrence of activities, while the portfolio of industrial projects has reduced its temporal action window.

- Finally, to reap the benefits of the method, it is necessary for some of the project actors to master it perfectly and make it intelligible to other stakeholders who have neither the time nor the inclination to learn it. This is what the eocen teams did in the two situations described, by designing and deploying the operational models on the supported projects.

- The last situation described highlights the ability of PPM solutions to enable many people to work according to tool-based processes, as long as they are correctly parameterized and fed by a clear, paced and animated process. This is also one of the strengths of eocen, via its DPS – Digital Portfolio Solutions – Department of Project Management Assistance, which provides project management services for the implementation and upgrading of PPM solutions to manage your project portfolios.

AND TO REFRESH YOUR MEMORY…

THE METHOD’S PREREQUISITES

The essential prerequisite for EVM is the existence of coherent, compatible project structures, in particular the WBS and CBS.

THE INDICATORS USED

Earned value management is based on the following indicators, whose names, calculation methods and, above all, concrete meaning must be remembered!

BUDGET

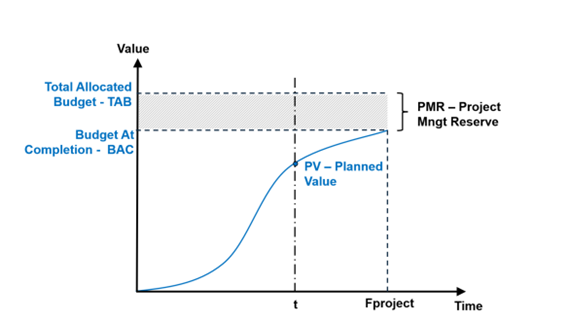

- BAC: Budget at completion

- PMR: Project Management Reserves

- TAB: Total Allocated Budget: TAB = BAC + PMR

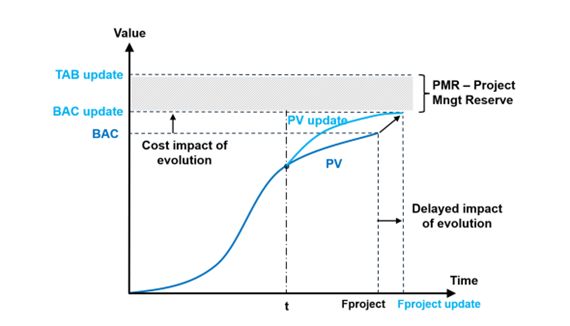

Note 1: The BAC is not set in stone. It is regularly updated by integrating the changes decided on for the project. This is obviously crucial for industrial projects that are subject to numerous changes.

EVM PARAMETERS

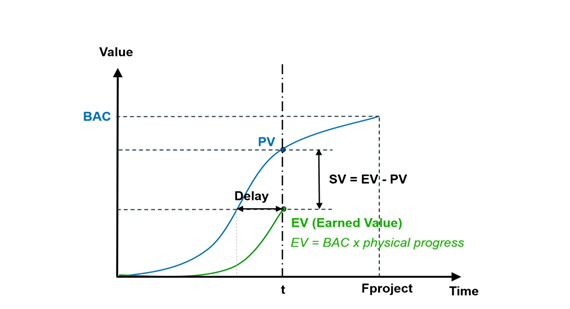

- PV: Planned Value. This is the value expected to be acquired during the project.

- EV: Earned Value defined as the budgeted value of the work carried out at the progress status date. EV = ∑ (Task budget x Task progress)

- AC: Actual costs

Note 2: 0-100, 0-50-100, equivalent units, intermediate milestones, expert judgement, etc. There are a wide variety of rules for calculating physical progress. It’s up to the project team to set the rules as early as possible… and stick to them.

Note 3: Expenditure is not earned value: EV is not AC. If this were the case, there would be no need for project managers!

VARIANCES AND PERFORMANCE INDICATORS

- SV: Schedule Variance: SV = EV – PV

- SPI: Schedule Performance Index: SPI = EV/PV

- CV: Cost Variance: CV = EV – AC

- CPI: Cost Performance Index: CPI = EV/AC

PROJECTION AT THE END

- RTC: Remaining To Complete: Estimated after complete review of remaining expenditure

- EAC: Estimate At Completion calculated according to several possible formulas: – EAC = AC + RTC- EAC = BAC/SPI- EAC = AC + (BAC-EV)/CPI.SPI

Note 4: In the figure above, EAC is greater than BAC. When a project cannot finance its cost overruns, it dips into its management reserves (PMR).

Note 5: There is a fundamental difference between the three EAC calculation formulas given above. The first is based on the notion of remaining work, which implies a complete review of the remaining expenditure, which is very tedious but generally more coherent if carried out rigorously. The next two, on the other hand, are based on an extrapolation of the project’s current situation, which generally leads to a less precise result, but one that is immediate and easy to deploy.

For further